Saturday, December 15, 2007

A sea of pain

This Economist Magazine article confirms my personal experience that value investing is in a sea of pain at the moment. The reasons are quite different from the last time (during the dotcom era) when value investing was in the doldrums. This time around, people are not full of euphoria about the prospects of growth stocks -- they are just getting increasingly gloomy of value stocks which seem to be getting cheaper by the minute.

Friday, November 23, 2007

Seasonal trades in stocks

Readers of this blog have seen my discussions of various seasonal trades in commodities futures (e.g. see this article). Recently, Mark Hulbert of the NYTimes drew our attention to a seasonal trade in stocks. The strategy is very simple: each month, buy a number of stocks that performed the best in the same month a year earlier, and short the same number of stocks that performed poorest in that month a year earlier. The average annual return is more than 13% before transaction costs, and since it is market neutral, this already considerable return can be leveraged to 2 or 3 times higher. Also, since it turns over the stocks only once a month, transaction costs should not be a major problem. The strategy was developed by Profs. Steven Heston and Ronnie Sadka, and details can be found online here. Besides its simplicity, the strategy is not as affected by survivorship bias in the data set as a mean-reverting strategy, since survivorship bias would tend to lower its backtest performance by excluding very poorly performing stocks that we would short. All in all, it seems to be a market neutral strategy made for retail trading!

Saturday, October 27, 2007

Economist article on quant funds

The media seems to have an endless fascination with quant funds. Here is the latest article from the Economist magazine, summarizing the postmortem published by several researchers. (Hat tip, once again, to reader Mr. J. Rigg.)

The key points are as follows:

1) Quant funds are now becoming the primary market makers in many securities, which normally would provide liquidity and decrease volatility.

2) Unlike ordinary market makers, however, quant funds are highly leveraged.

3) Because of the high leverage, in the face of large losses these market-making quant funds are forced to liquidate their assets instead of buying them, thus behaving in a way opposite to ordinary market makers just when the need for liquidity is direst.

4) Thus quant funds are actually contributing to instability of the market despite their apparent market-making function.

Fortunately, when all else has gone wrong, there is alway Mr. Bernanke to count on ...

The key points are as follows:

1) Quant funds are now becoming the primary market makers in many securities, which normally would provide liquidity and decrease volatility.

2) Unlike ordinary market makers, however, quant funds are highly leveraged.

3) Because of the high leverage, in the face of large losses these market-making quant funds are forced to liquidate their assets instead of buying them, thus behaving in a way opposite to ordinary market makers just when the need for liquidity is direst.

4) Thus quant funds are actually contributing to instability of the market despite their apparent market-making function.

Fortunately, when all else has gone wrong, there is alway Mr. Bernanke to count on ...

Sunday, October 07, 2007

Emerging markets stocks vs. natural resource stocks

Emerging market stocks have been reaching new highs almost everyday (see this article in the Economist magazine), and the natural resource sector has been on a tear as well. Given the giddy valuations of both sectors, which one is a better relative buy at this point? For those of you who have been following the IGE-EEM spread that I proposed before, its value is at an all-time-low these days -- it was at -6.77 standard deviations. Given their historical cointegration, I wouldn't be surprised if it will revert to a more sane value in the near future.

Saturday, October 06, 2007

How a mean-reversion strategy performed in August

Prof. Andrew Lo and Mr. Amir Khandani at MIT recently wrote a paper on "What Happened To The Quants In August 2007?" (Hat tip to my reader Mr. J. Rigg for the article). Most of their conclusions confirm what many observers already suspected: that the loss is likely due to the simultaneous forced liquidation of portfolios holding similar positions by various quantitative funds. What is noteworthy, however, is that they constructed a mean-reversion strategy and observed what happened to it during August. This strategy is very simple: buy the stocks with the worst previous 1-day returns, and short the ones with the best previous 1-day returns. Despite its utter simplicity, this strategy has had great performance since 1995, ignoring transaction costs. The Sharpe ratio was an astounding 53.87 in 1995, gradually decreasing to 4.47 in 2006. However, the strategy also had a disastrous few days on August 7-9, suffering a cumulative (arithmetic) return of -6.85% in those 3 days. Then on August 10, it rebounded, like the rest of the quant funds, with a return of 5.92%, almost reversing all of its previous losses. For me, this experiment reveals three interesting points: 1) a simple price factor seems to capture most of the performance of the complex factor models run by the gigantic hedge funds; 2) even technical mean-reverting factors suffer losses, not just momentum (growth) factors based on fundamentals; and 3) if one wants to avoid disasters and enjoy spectacular returns, even a one-day holding period is too long. I haven't done the experiment myself yet, but I bet that if we were to liquidate the portfolio at market close each day, not only would we avoid the loss of -6.85% in those 3 days, but would probably end up with a positive return of a similar magnitude!

Thursday, September 20, 2007

So how much did quantitative strategies actually lose last quarter?

The numbers have started to come in: Morgan Stanley lost $480MM last quarter due to quantitative trading -- about 10% of operating profits.

Wednesday, September 19, 2007

Hedge fund replication

I wrote about how hedge fund returns can be replicated with simple factor models. I just learn that IndexIQ, a company in Rye Brook, NY,

Monday, September 17, 2007

More discussion on returns, risk and leverage

Previously I discussed an important debate on whether it is better to increase a portfolio's return by taking on more risks (e.g. holding high-beta stocks), or by increasing leverage but holding low-risk assets. A reader Mr. F. Sudirga has kindly send me some other research papers supporting the conclusion that increasing leverage is the preferred way.

In a paper titled "Risk Parity Portfolios", Dr. Edward Qian at PanAgora Asset Management argued that a typical 60-40 asset allocation between stocks and bonds is not optimal because it is overweighted with risky assets (stocks in this case). Instead, to achieve a higher Sharpe ratio while maintaining the same risk level as the 60-40 portfolio, Dr. Qian recommended a 23-77 allocation while leveraging the entire portfolio by 1.8. The stock-bond dichotomy is for illustration only -- the results can be improved further by including other asset classes such as commodities.

The only reservation I have with all this enthusiasm with increasing leverage is one that many risk-managers are aware of: most of the research uses concepts such as standard deviations to measure risk. But as the LTCM debacle as well as the recent subprime mortgage meltdown has reminded us, risky events have fat-tailed distributions. Therefore, one should be very wary of using standard deviation as the sole determinant of leverage.

In a paper titled "Risk Parity Portfolios", Dr. Edward Qian at PanAgora Asset Management argued that a typical 60-40 asset allocation between stocks and bonds is not optimal because it is overweighted with risky assets (stocks in this case). Instead, to achieve a higher Sharpe ratio while maintaining the same risk level as the 60-40 portfolio, Dr. Qian recommended a 23-77 allocation while leveraging the entire portfolio by 1.8. The stock-bond dichotomy is for illustration only -- the results can be improved further by including other asset classes such as commodities.

The only reservation I have with all this enthusiasm with increasing leverage is one that many risk-managers are aware of: most of the research uses concepts such as standard deviations to measure risk. But as the LTCM debacle as well as the recent subprime mortgage meltdown has reminded us, risky events have fat-tailed distributions. Therefore, one should be very wary of using standard deviation as the sole determinant of leverage.

Monday, August 27, 2007

Whatever happened to the XLE-USO spread?

Recently Mr. Teetor, a subscriber of mine, has posted an enthusiastic comment on trading the XLE-USO spread that I suggested. While Mr. Teetor has a lot of success trading this spread, I must say that I have lost faith in the cointegrating characteristic of this spread because of two reasons:

The two reasons are, I believe, intertwined. Unlike GLD (part of a much more cointegrating spread that I discussed and tracked in my premium content area), USO does not actually hold commodity assets in its portfolio. It holds nearby futures contracts in oil. When the USO fund started trading in April 2006, its price per share was very close to the spot oil price. Now, however, USO is trading at about $53, while spot oil price is at about $70.6. How can a fund that is supposed to reflect oil price diverge so much from it after a year and 5 months? The reason is that the oil futures market has been in contango since 2005 or so, i.e. far month futures costs more than the nearby contracts, which results in negative roll-yield for long position in oil futures. In the historic period from which the XLE-USO cointegration relation was established, oil futures market exhibited backwardation: far month futures cost less than nearby futures. This regime shift partially explains the breakdown of the cointegration relation in the present out-of-sample period.

The lesson I have learned from all these is to avoid analyzing cointegration relation when either side of a spread involves futures contracts at different points of the forward curve, at least on a time-scale when the shape of that curve might change. (I argued before that XLE, the other side of the spread, can be modeled as an average over the entire forward curve.) Meanwhile, the fund manager of USO would really have done investors a much better favor by getting their hands dirty, leasing some oil storage tanks and buying some real oil assets rather than keeping their hands clean and dealing in futures contracts alone. After all, retail investors like myself can just as easily buy oil futures ourselves, but we can't very well go out and rent an oil tank.

Thursday, August 23, 2007

CIO Magazine Innovation and IT Strategy blog

Ms. Elana Varon who writes the CIO Magazine's Innovation and IT Strategy blog quoted me today in saying that some quantitative investment models are over-engineered. This old article of mine is an elaboration of my view on this.

Wednesday, August 22, 2007

The Perils of Momentum Strategies

Not so long ago I was an agnostic with respect to choosing between mean-reverting and momentum models: I felt that depending on the particular model or environment, each can be profitable. Lately, however, I am increasingly skeptical about the long-term profitability of momentum models. The main reason is the increasing competition among traders, algorithmic or otherwise.

As I mentioned in my previous post, when more and more traders decide to adopt mean-reverting strategies, all they do is to eliminate the trading opportunity. The market becomes efficient, and nobody makes any money, but nobody loses either. In contrast, when more and more traders decide to adopt momentum strategies, the momentum will be established sooner and sooner. For e.g. in the case of event-driven strategies which are mostly momentum-based, the new equilibrium price will have been established almost instantaneously after the event is publicly disclosed. Under this circumstance, any momentum trades that are entered just a little bit late will not only suffer zero profit, but will likely suffer losses as mean-reversion almost inevitably takes over. But how soon do we need to enter in order to avoid this fate? (It can't be too soon either because often a trend need to be established first in order to trigger an entry signal.) It is unfortunately a moving target as competition increases: 1 day earlier might work now, but may not be sufficient a few months from now. (The exit trade also suffers the same problem, as we don't know how long the momentum will last.) It is a dangerous game to play.

Indeed, time is often a friend of the mean-reversion trader: the longer s/he waits, perhaps the more profitable the trading opportunity. And if s/he enters too early and suffers a loss, s/he can always double the position. As I explained in a previous article, stop-loss should generally not be applied to mean-reverting trades on a short time-scale. So even if the trader does not double-up the position, an eventual re-couping of the loss is more than likely. On the other hand, time is an enemy of the momentum trader: if s/he loses the first-mover advantage and suffers heavy loss, I argued in that article that a stop-loss is advised, and thus the loss is forever locked-in.

Given this asymmetry, it is no wonder that algorithmic traders have been warning me long ago that it is hard to find a profitable momentum trade. And I was silly enough not to pay heed to them until now.

As I mentioned in my previous post, when more and more traders decide to adopt mean-reverting strategies, all they do is to eliminate the trading opportunity. The market becomes efficient, and nobody makes any money, but nobody loses either. In contrast, when more and more traders decide to adopt momentum strategies, the momentum will be established sooner and sooner. For e.g. in the case of event-driven strategies which are mostly momentum-based, the new equilibrium price will have been established almost instantaneously after the event is publicly disclosed. Under this circumstance, any momentum trades that are entered just a little bit late will not only suffer zero profit, but will likely suffer losses as mean-reversion almost inevitably takes over. But how soon do we need to enter in order to avoid this fate? (It can't be too soon either because often a trend need to be established first in order to trigger an entry signal.) It is unfortunately a moving target as competition increases: 1 day earlier might work now, but may not be sufficient a few months from now. (The exit trade also suffers the same problem, as we don't know how long the momentum will last.) It is a dangerous game to play.

Indeed, time is often a friend of the mean-reversion trader: the longer s/he waits, perhaps the more profitable the trading opportunity. And if s/he enters too early and suffers a loss, s/he can always double the position. As I explained in a previous article, stop-loss should generally not be applied to mean-reverting trades on a short time-scale. So even if the trader does not double-up the position, an eventual re-couping of the loss is more than likely. On the other hand, time is an enemy of the momentum trader: if s/he loses the first-mover advantage and suffers heavy loss, I argued in that article that a stop-loss is advised, and thus the loss is forever locked-in.

Given this asymmetry, it is no wonder that algorithmic traders have been warning me long ago that it is hard to find a profitable momentum trade. And I was silly enough not to pay heed to them until now.

Tuesday, August 21, 2007

Further debate on factor models

A reader from a hedge fund (who wishes to remain anonymous) sends me some thoughtful comments about factor models. He has graciously allowed me to reprint them here:

"With regards to your blog entry, 'The Robin Hood regime': this weekend I was actually also thinking about the philosophy behind factor models which you allude to in the post. I am wondering if you have any other thoughts as to what service factor models provide? Relegating them to 'just arrogant bets on the correctness of the managers' convictions' isn’t completely intellectually satisfying to me.

"With regards to your blog entry, 'The Robin Hood regime': this weekend I was actually also thinking about the philosophy behind factor models which you allude to in the post. I am wondering if you have any other thoughts as to what service factor models provide? Relegating them to 'just arrogant bets on the correctness of the managers' convictions' isn’t completely intellectually satisfying to me.

I look at factors as such: the returns I get for exposure to various factors can come either because the market is inefficient and systematically misprices those factors (alpha), and/or because I am providing some service via the exposure (and collecting some kind of risk premium associated with that service). My question #1 to you is, are you convinced that all of the returns to factor models are indeed simply from risk premiums and not alpha? If alpha exists, it’s less clear that a service needs to be provided to the market, at least to me.

However, let’s assume (as I believe your boss did) that in the long run, the market is efficient. Then, you will be compensated for factor exposure only by bearing some risk or providing some service. In my mind, some particular conviction of a manager doesn’t necessarily qualify for a risk factor in and of itself - I think we agree on that point. But are there possible fundamental, valuation-based explanations behind these factors? Perhaps low VALUE companies are generally those companies with bad recent performance but which are expected to turnaround / mean-revert (as you somewhat suggest in your post) and the risk you bear when buying a low P/E company is “turnaround risk”. Or perhaps high MOMENTUM companies are companies riding an industry trend and you are bearing “trend continuation risk”. So, my question #2 to you is, are you convinced that there are no such explanations?

If factor models do indeed work, it seems to me that there must either be real risks behind the factors, or alpha, or both."

And here is my response:

"I believe the service that some value factors provide is the efficient allocation of capital to those companies that deserve them, just like any value investors do. In this case, the factors hope to identify these companies faster than humans can, and therefore bring capital to them sooner. I have no argument with these factors as they also provide liquidity, albeit on a longer time-scale. However, with regard to various momentum factors, they are in fact just betting on certain behavioral characteristics of investors, or on the slow dissemination of news, etc. You can argue that they provide a service by improving the efficiency with which information about companies disseminate. But the problem is that once everybody are using these momentum factors, the market becomes efficient and any further bets generate losses.So I am quite willing to accept that many of these (momentum) factors represent alpha, but these factors are generating more losses as more investors employ them. I am also willing to accept that many of the (value) factors represent risk premia. As more investors employ these, the profit goes to zero, but fortunately not negative as the risk also disappears."

Sunday, August 19, 2007

The "failed" factors have reverted

As I said in my CNBC interview, investors just got to be patient with the factor models. Sure enough, we are seeing reports that the large drawdown suffered by these models has already reverted as of Friday.

Saturday, August 18, 2007

The Robin Hood regime

It has become apparent to me in the last month that there has been a massive transfer of wealth from the gigantic hedge funds running factor models to many day-traders with accounts less than $10M. I call this the Robin Hood regime (regime being a common technical term referring to a particular trading environment, as in "this is a mean-reverting regime"). Many, many day-traders that I heard from have had one of their best months in a long while. Is this just luck, or is there a deeper explanation?

I believe that there is a philosophical difference between factor models and many of the mean-reverting strategies that day-traders like to employ, a difference that works to the day-traders' favor. I recall a wise musing from one of my former bosses: he believes that a trading strategy will be profitable in the long run only if it performs a service for other market participants. The service that mean-reverting strategies performs is the provision of liquidity, in particular, short-term liquidity. What service does factor models provide? They seem to be just arrogant bets on the correctness of the managers' convictions. For e.g. I believe that stocks with good earnings will rise in value. Or, I believe that stocks with increasing price momentum will continue in that momentum. True, most of the time the convictions of the best managers are correct, and many of these convictions are actually mean-reverting as well (for e.g. the "value" factors). But on average, a factor model may take away as much liquidity from the market as it provides. And sooner or later, some of these convictions are wrong. Maybe not wrong for very long, but long enough to cause investors' panic. This may be part of what we are seeing recently.

Now am I advocating that every gigantic fund simply just switch from factor models to pure mean-reverting strategies? No: that would be impractical when the portfolios involved are in the tens of billions. If everybody run mean-reverting strategies, there will hardly be any mean-reversion left to profit from. (Look what happened to pair-trading in the last few years.) When you are an investor in a multi-billion fund, and you expect the fund to deliver higher returns than the risk-free rate, you just have to accept that high short-term returns volatilities will be part of the bargain, just like any long-term investments.

I believe that there is a philosophical difference between factor models and many of the mean-reverting strategies that day-traders like to employ, a difference that works to the day-traders' favor. I recall a wise musing from one of my former bosses: he believes that a trading strategy will be profitable in the long run only if it performs a service for other market participants. The service that mean-reverting strategies performs is the provision of liquidity, in particular, short-term liquidity. What service does factor models provide? They seem to be just arrogant bets on the correctness of the managers' convictions. For e.g. I believe that stocks with good earnings will rise in value. Or, I believe that stocks with increasing price momentum will continue in that momentum. True, most of the time the convictions of the best managers are correct, and many of these convictions are actually mean-reverting as well (for e.g. the "value" factors). But on average, a factor model may take away as much liquidity from the market as it provides. And sooner or later, some of these convictions are wrong. Maybe not wrong for very long, but long enough to cause investors' panic. This may be part of what we are seeing recently.

Now am I advocating that every gigantic fund simply just switch from factor models to pure mean-reverting strategies? No: that would be impractical when the portfolios involved are in the tens of billions. If everybody run mean-reverting strategies, there will hardly be any mean-reversion left to profit from. (Look what happened to pair-trading in the last few years.) When you are an investor in a multi-billion fund, and you expect the fund to deliver higher returns than the risk-free rate, you just have to accept that high short-term returns volatilities will be part of the bargain, just like any long-term investments.

Tuesday, August 14, 2007

CNBC Interview video

Here is the link to my interview on why quantitative models are losing money of late:

Monday, August 13, 2007

CNBC interview

Folks, I will be appearing on CNBC tomorrow (Tue, August 14) for a live interview about quantitative trading with Maria Bartiromo. The segment will be aired around 3:20 pm ET.

A reader's comment on quant funds' losses

A reader of mine (who wish to remain anonymous) pointed out that most of the losses seem to come from low-frequency trading models, while high frequency models continue to perform superbly. This also confirms my own experience. My enthusiasm for high frequency trading was expressed previously here and here.

An update on why quantitative funds are losing money recently

A story just came through Dow Jones newswire ("How Black Boxes Became Pandora's Boxes" by Spencer Jakab) suggesting that recent losses are due to factor models gone bad. Given my expressed distaste for such models, that should have been my first guess instead of blaming the "exotic" models!

Why are quantitative funds losing money these days?

The New York Times today has an article about several well-known quantitative hedge funds incurring significant losses in recent months. I was quoted in saying that traders running similar quantitative models could contribute to market volatility. This is certainly true if the strategies are trend-following. What puzzles me, however, is that most statistical arbitrage strategies are mean-reverting: they buy during investors' panic, and sell during investors' euphoria, and should be richly rewarded in this volatile market by providing sorely needed liquidity. And indeed, from my own experience as well as hearing from other traders, mean-reverting strategies are performing very well recently. So where did those losses come from? My guess is that, as I have observed before, many traditional stat arb strategies are getting boring and generating diminishing returns, and therefore many of the quantitative researchers are driven (by their own professional pride or their bosses) to come up with more exotic and higher-return strategies that ultimately may not stand the test of time. For us quants, remembering Occam's razor and that our job is to generate returns as opposed to producing brilliant mathematical models is often a hard lesson to learn.

Thursday, August 02, 2007

Currency trading resources

For those of you who are into currency trading, this blog looks interesting. You can also subscribe to a free daily email newsletter called "The Daily Pfennig" from www.everbank.com.

Monday, July 16, 2007

More on news-driven trading

For readers who are interested in news-driven trading, here is another article. This article pointed out a contrarian view offered by Richard Oldfield, a fund manager, who says “price movements in response to news are exaggerated, providing an opportunity to those who do not base too much on what has happened in the last hour or 24 hours.” [my italics] I am not sure whether Mr. Oldfield's statement is based on any statistical research or not -- as far as I can ascertain, his book "Simple But Not Easy” cannot be purchased anywhere in North America. However, I should point out that this statement is in contradiction to an abundance of research done on Post Earnings Annoucement Drift (PEAD): the phenomenon that stocks with positive earnings news continue to trend up for a long time. Furthermore, if indeed price movements in response to news are exaggerated (contrary to the findings of PEAD), it would seem to suggest a reversal trade rather than suggesting that the news can be ignored!

Thursday, June 28, 2007

Fair value of currencies

In the same issue of the Economist magazine I cited previously, there is an article about the valuation of currencies based on 13 quantitative models that Morgan Stanley developed. They found that the most overvalued currency (against the US dollar) is the New Zealand dollar, while the most undervalued currency is the Japanese Yen.

What about the Chinese Yuan that arouses much hoopla in Congress? The models found it to be almost exactly fairly valued.

What about the Chinese Yuan that arouses much hoopla in Congress? The models found it to be almost exactly fairly valued.

Wednesday, June 27, 2007

News-driven algorithmic trading

There is an article about algorithmic trading in the latest issue of the Economist magazine, where it says that one-third of all stock trades in the US are due to algorithmic trading. This should not surprise us. What is more interesting is its mention of the electronically tagged news products that are coming out of Dow Jones and Reuters, which purportedly enable computers to buy or sell stocks immediately upon the release of a news item. The data suppliers regard these news products as some kind of secret high-tech weapons: "Dow Jones claims the business is so secretive that it cannot divulge details of customers." Is this hype justified?

Actually, to get a taste of news-driven trading, you don't need to pay a hefty fee to buy one of these products. You can just monitor the regularly scheduled economic news release (consumer confidence, new homes sales, crude inventories, etc.), trade the relevant futures, and proceed to make millions.

The fact that most of us who monitor these economic news releases haven't yet made our millions is an indication whether these news products will help you do the same. The information contained in the news is often difficult to interpret. Even the initial price reaction to the news may be wrong, leading to swift reversal after an apparent initial trend. And finally, what's wrong with scanning for sudden price movemenets, and then check for possible news to confirm that the price movement is due to the release of new information?

Actually, to get a taste of news-driven trading, you don't need to pay a hefty fee to buy one of these products. You can just monitor the regularly scheduled economic news release (consumer confidence, new homes sales, crude inventories, etc.), trade the relevant futures, and proceed to make millions.

The fact that most of us who monitor these economic news releases haven't yet made our millions is an indication whether these news products will help you do the same. The information contained in the news is often difficult to interpret. Even the initial price reaction to the news may be wrong, leading to swift reversal after an apparent initial trend. And finally, what's wrong with scanning for sudden price movemenets, and then check for possible news to confirm that the price movement is due to the release of new information?

Friday, June 22, 2007

Pair trading stocks and the life-cycle of strategies

I have discussed in various articles trading the spreads between pairs of ETF’s, or between a basket of stocks against an ETF using cointegration technique. There is, however, a glaring omission, as I haven’t yet mentioned the classic statistical arbitrage strategy: pair-trading stocks.

There are pros and cons on applying cointegration to pair-trading stocks. On the pro side: because of the large number of stocks, we can enjoy a highly diversified portfolio that improves the validity of our results. Even if a number of spreads fail to cointegrate going forward, we can count on a larger number of spreads that still do. (For e.g. my USO-XLE spread fell apart, while GLD-GDX spread is still tightly cointegrated.) There are 2 main cons: 1) stocks are subject to various specific risks which may render our purely statistical model useless, especially in M&A situations. Therefore it is customary to remove such stocks from our portfolio when they are involved in special situations – however, by the time the news is public we may have incurred substantial loss already; also 2) because of the technique’s long history, it became known to many hedge funds and indeed students of finance, and therefore pair trading stocks has not been very profitable, especially in the period 2003-2005. Here I plotted the excess returns of the strategy as applied to US bank stocks from 20010102-20041231. (Excess returns means credit interest on margin balance is not included.)

Interestingly, when a strategy becomes too popular and less profitable, many traders start to abandon it, or at least reduce their trading capital invested in the strategy. After a while, its popularity decreases, and the profitability recovers! This life-cycle of strategies reveals itself as mean-reversion of strategies, on top of mean-reversion of stock prices. In our case, this strategy recovery starts in 2005, and is still in full-force. Here I plotted the excess returns of the strategy as applied to US bank stocks from 20050103 to 20070531:

The average annual excess return in 2005-now is about 7.7% (on one-side of capital), and the Sharpe ratio is 0.8. Since I have applied the technique on only one industry group, diversification is limited and therefore the Sharpe ratio is low. For the interested readers, they can attempt to apply this technique to more industry groups and perhaps generate a higher Sharpe ratio. Even with just one industry group, this trading strategy may be a good complement to a portfolio heavy on trend-following strategies and therefore require a reversal model to smooth out the returns.

I have started a model portfolio in my subscription area to demonstrate this strategy which will be updated daily around 3pm ET. Other details of the strategy will be detailed in an accompanying article there as well.

The effect of terrorism on forex trading

Here is an interesting and thoughtful article, with reference to an academic study, on how terrorism affects forex trading.

Tuesday, June 12, 2007

A factor model that I can believe in

Some of you may remember that I preached about the uselessness of factor models in predicting short term return, and the unreliability of many exotic factors even for the long term. In particular, factor models are especially inaccurate in valuing growth stocks (i.e. stocks with low book-to-market ratio), as evidenced by such models' poor performance during the internet bubble. This is not surprising because most commonly used factors rely on historical sales or earnings measures to judge companies, while many growth stocks have very short history and little or no earnings to report. However, as pointed out recently by Barry Rehfeld in the New York Times, Professor Mohanram of Columbia University has devised a simple factor model that rely on 8 very convincing factors to score growth stocks. These factors are:

Interestingly, Prof. Mohanram pointed out that most of the out-performance of the high-score stocks occur around earnings announcements. Hence for those investors who don't like holding a long-short portfolio for a full year, they can just trade during earnings season.

One caveat of this research is that it was based on 1979-99 data (at least for the preprint version that I read). As many traders have found out, strategies that work spectacularly in the 90's don't necessarily work in the last few years. At the very least, the returns are usually greatly diminished. In the future, I hope to perform my own research to see whether this strategy is still holding up with the latest data.

- Normalized return on assets.

- Normalized return on assets based on cash flow.

- Cash flow minus net income. (i.e. negative of accrual.)

- Normalized earnings variability.

- Normalized sale growth variability.

- Normalized R&D expenses.

- Normalized capital spending.

- Normalized advertising expenses.

Interestingly, Prof. Mohanram pointed out that most of the out-performance of the high-score stocks occur around earnings announcements. Hence for those investors who don't like holding a long-short portfolio for a full year, they can just trade during earnings season.

One caveat of this research is that it was based on 1979-99 data (at least for the preprint version that I read). As many traders have found out, strategies that work spectacularly in the 90's don't necessarily work in the last few years. At the very least, the returns are usually greatly diminished. In the future, I hope to perform my own research to see whether this strategy is still holding up with the latest data.

Monday, May 14, 2007

Platinum vs. Gold

Saturday, May 05, 2007

Recap: Australian dollar futures seasonal trade

Yesterday was the exit of the Australian dollar futures seasonal trade which I discussed in my premium content. It incurred a loss of $920 per contract, despite a 12-year winning streak previously. This may be the peril of a trade that is not based on any fundamental rationale that I know of, as well as an in-sample bias that I alluded to in my previous article. I will keep it on my watchlist for another year.

By the way, due to a technical glitch, my previous article on seasonality in commodities futures was not sent to many subscribers, so here is the link.

By the way, due to a technical glitch, my previous article on seasonality in commodities futures was not sent to many subscribers, so here is the link.

Wednesday, May 02, 2007

Are claims of seasonality in commodity futures markets "fraudulent "?

I have written about several commodities futures seasonal trades (e.g. PL-GC here, and RT here) recently, and while I was researching another such trade I came upon this webpage from the Commodity Futures Trading Commission. It says, in no uncertain terms,

" The Commodity Futures Trading Commission (CFTC) warns consumers to be alert to possible fraudulent claims that they can profit on commodity futures or options trading as a result of changes in the prices of physical commodities based on seasonal weather patterns or other well-known events."

It goes on to say that

"Futures and options markets adjust very quickly to news events and announcements, and by the time salesmen come calling, the opportunity to profit from such news is gone."

Whoa, this certainly got my attention! Since I am not a journalist, I don't normally go around challenging claims made by the United States government. But if this statement, which is basically the efficient market hypothesis, is generally true, then all of us traders should just pack up and go home. Now whether or not the efficient market hypothesis is true is subject to much academic debate. But is it right for the government to state definitively that this hypothesis is true, and that all claims otherwise are "fraudulent"?

Political arguments aside, I think that the commodities market may have more arbitrage opportunities (i.e. less efficient) than the stock market. Perhaps this is because there are more participants in the commodities markets that are not speculators, particularly for "consumption" commodities such as oil and gas.

This is not to say that every seasonal pattern that we have backtested is necessarily going to repeat itself. Many of these patterns occur only once a year, and there are just so many years that we can use for our backtest, and needless to say, most of them are "in-sample". My practice is to paper-trade the pattern for at least one year going forward as an "out-of-sample" test, especially if the pattern is not supported by a strong fundamental rationale (like the Australian dollar trade that I talked about in my premium content area.) Furthermore, by publishing my backtest results on this blog, any future repeat of the pattern can indeed be regarded as out-of-sample, increasing our confidence in them.

My own interest in researching seasonality in commodities market was (hopefully) not piqued by the kind of snake-oil salesman that CFTC warns us about. About a year or so ago, I attended a talk given by Dr. David Eliezer at Columbia University's Financial Engineering seminar. The topic is "Structure and Behavior of Commodities Markets" in which he outlined various seasonal patterns that persist in the futures markets. Dr. Eliezer was formerly the chief quantitative researcher at Goldman Sachs' commodities group. Given this academic respectability, I certainly feel emboldened to enter into the debate!

Political arguments aside, I think that the commodities market may have more arbitrage opportunities (i.e. less efficient) than the stock market. Perhaps this is because there are more participants in the commodities markets that are not speculators, particularly for "consumption" commodities such as oil and gas.

This is not to say that every seasonal pattern that we have backtested is necessarily going to repeat itself. Many of these patterns occur only once a year, and there are just so many years that we can use for our backtest, and needless to say, most of them are "in-sample". My practice is to paper-trade the pattern for at least one year going forward as an "out-of-sample" test, especially if the pattern is not supported by a strong fundamental rationale (like the Australian dollar trade that I talked about in my premium content area.) Furthermore, by publishing my backtest results on this blog, any future repeat of the pattern can indeed be regarded as out-of-sample, increasing our confidence in them.

My own interest in researching seasonality in commodities market was (hopefully) not piqued by the kind of snake-oil salesman that CFTC warns us about. About a year or so ago, I attended a talk given by Dr. David Eliezer at Columbia University's Financial Engineering seminar. The topic is "Structure and Behavior of Commodities Markets" in which he outlined various seasonal patterns that persist in the futures markets. Dr. Eliezer was formerly the chief quantitative researcher at Goldman Sachs' commodities group. Given this academic respectability, I certainly feel emboldened to enter into the debate!

Wednesday, April 25, 2007

Recap: Gasoline futures seasonal trade

The gasoline futures seasonal trade that I mentioned in a previous post and discussed in details in my premium content area reached its exit today. It has been profitable for at least 11th consecutive years: the profit this year is $4,321.80 per contract of RT.

Friday, April 20, 2007

Recap: Platinum-gold spread trade

The platinum-gold spread trade that I discussed is once again profitable this year. If a trader entered the positions near the close on February 26 and exited the positions near the close on April 19, the profit would have been about $6,610 this time. However, I did made a calculation mistake when I plotted the historical profit graphs before. So here it is again:

The maximum draw-down experienced in the last 7 years is -$4,860. The average profit is $3,064, the maximum profit is $7,320 and the maxmium loss is -$540.

The maximum draw-down experienced in the last 7 years is -$4,860. The average profit is $3,064, the maximum profit is $7,320 and the maxmium loss is -$540.

Monday, April 16, 2007

Out-of-sample test on cointegrating basket of stocks

An anonymous reader "L" posted some thoughtful objections to the way I constructed the basket of stocks that is supposed to cointegrate with XLE. His main objection is that even though my basket shows cointegration with XLE in-sample, this is likely to fail out-of-sample. Actually, I agree with him that the strong statistical relationship discovered in-sample is most likely going to be weakened out-of-sample, most often because the nature of the component stocks is always changing, due to various corporate events (management change, restructuring, change of strategic direction, etc.). However, from a practical trading point of view, I believe that the relationship should not be weakened to the point that the trading signals become spurious, at least over a time-scale of a trade which is several months to half-a-year at most.

To demonstrate this, let's break up the dataset over 2 periods: 20010522 - 20030123 and 20030124 - 20070403. In the first in-sample period (with 1,000 data points), we pick our 10 stocks to form the basket, and in the second out-of-sample period we see how well it cointegrates with XLE, and we observe how the spread behaves. I found that in the first period, the t-statistic for cointegration is -3.61934140, indicating the basket cointegrates with over 95% probability. No surprise here. Here is a plot of the spread in this period:

Now, let's find out what happens in the out-of-sample period. Here the t-statistic is just -2.72, whereas the critical value for cointegration at 90% probability is -3.03. So indeed the basket fails to cointegrate at the 90% confidence level. Does that mean our trades will therefore be losing out-of-sample? Not necessarily. Take a look at the behavior of the spread out-of-sample:

Even though it is not nicely symmetric around zero as in the in-sample period, the spread is still clearly bounded around zero. If the basket completely falls out of cointegration with XLE, it will show a random drift away from zero as time goes on.

To show that this is not just good luck based on our specific in-sample period, let's try a longer in-sample period of 1500 days (shorter in-sample period won't work, because we need a minimum of 1,000 data points here to construct a good reliable basket.) Here the cointegration t-statistic is a bit worse, at -2.62. If we look at the spread:

Once again, we see that the spread is bounded, not wandering off to infinity. So in conclusion, I maintain that my method of constructing the basket is good for practical trading, though not necessarily guaranteeing as high a statistical confidence level as might be indicated in the in-sample period.

To demonstrate this, let's break up the dataset over 2 periods: 20010522 - 20030123 and 20030124 - 20070403. In the first in-sample period (with 1,000 data points), we pick our 10 stocks to form the basket, and in the second out-of-sample period we see how well it cointegrates with XLE, and we observe how the spread behaves. I found that in the first period, the t-statistic for cointegration is -3.61934140, indicating the basket cointegrates with over 95% probability. No surprise here. Here is a plot of the spread in this period:

Now, let's find out what happens in the out-of-sample period. Here the t-statistic is just -2.72, whereas the critical value for cointegration at 90% probability is -3.03. So indeed the basket fails to cointegrate at the 90% confidence level. Does that mean our trades will therefore be losing out-of-sample? Not necessarily. Take a look at the behavior of the spread out-of-sample:

Even though it is not nicely symmetric around zero as in the in-sample period, the spread is still clearly bounded around zero. If the basket completely falls out of cointegration with XLE, it will show a random drift away from zero as time goes on.

To show that this is not just good luck based on our specific in-sample period, let's try a longer in-sample period of 1500 days (shorter in-sample period won't work, because we need a minimum of 1,000 data points here to construct a good reliable basket.) Here the cointegration t-statistic is a bit worse, at -2.62. If we look at the spread:

Once again, we see that the spread is bounded, not wandering off to infinity. So in conclusion, I maintain that my method of constructing the basket is good for practical trading, though not necessarily guaranteeing as high a statistical confidence level as might be indicated in the in-sample period.

Saturday, April 07, 2007

Hedging isn't always better

Many of the strategies I wrote about in this blog are market-neutral strategies: long one instrument and short another one as a hedge. In many hedge funds, these are the only strategies that are allowed: investors imagine that only market-neutral hedge funds can deliver consistent returns in bull and bear markets alike, and the typically smaller drawdowns experienced by such funds allow them to obtain higher leverage from their prime brokerages. However, over the years I have become convinced that this bias in favor of market neutral strategies is misplaced in several ways.

First off, it is a bit silly to work hard to find a market-neutral strategy so that we can have a smaller drawdown so that we can increase its leverage to boost its return. After all these leveraging, the drawdown is often back to the same level as a long-only strategy! Why not just run a long-only strategy at a lower leverage, but that is often simpler in design and that incurs lower transaction costs (since there is only one-side of the trade to execute)?

Secondly, there is a misconception that long-only strategies will surely lose money in bear markets. This is probably true when you are holding overnight -- but long-only day-trading strategies are often profitable in both bull and bear markets.

Thirdly, there are strategies where only the long trades work. A simple example is a strategy that buys an index at its 10-day low, and exit when... well, there are multiple ways to exit and most of them work! If you try the mirror image of this strategy, i.e. short an index at its 10-day high, it works far less well. This simply reflects the positive mean return of the equity market, and why not take advantage of that?

Finally, related to the third point, sometimes the short hedge fails simply because the short instrument is actually quite different in nature than the long one, despite their superficial similarity. An example is provided by Mr. Sandy Fielden at Logical Information Machines. There is a usually profitable trade where you long a May gasoline futures contract and simultaneously short a May heating oil contract in the spring. The logic is that as the weather gets warmer, the driving season will begin which drives the price of gasoline futures up, and the demand for heating will decrease which drives the price of heating oil futures down. This hedged trade is supposed to eliminate general energy market risk. However, the weather is sometimes unpredictable, and in 2005, this trade went quite wrong primarily because the winter lasted longer. On the other hand, if you only enter the long side of this trade, i.e. buy gasoline futures in the spring, it works like a charm every year in the past 10 years! (I have posted a detailed analysis of this long-only gasoline futures trade in my Premium Content area.)

Therefore, if you trade for yourself and not for some institutions with a mandate only for market-neutral strategies, there is no need to be bounded by the same rules that they have to play by.

First off, it is a bit silly to work hard to find a market-neutral strategy so that we can have a smaller drawdown so that we can increase its leverage to boost its return. After all these leveraging, the drawdown is often back to the same level as a long-only strategy! Why not just run a long-only strategy at a lower leverage, but that is often simpler in design and that incurs lower transaction costs (since there is only one-side of the trade to execute)?

Secondly, there is a misconception that long-only strategies will surely lose money in bear markets. This is probably true when you are holding overnight -- but long-only day-trading strategies are often profitable in both bull and bear markets.

Thirdly, there are strategies where only the long trades work. A simple example is a strategy that buys an index at its 10-day low, and exit when... well, there are multiple ways to exit and most of them work! If you try the mirror image of this strategy, i.e. short an index at its 10-day high, it works far less well. This simply reflects the positive mean return of the equity market, and why not take advantage of that?

Finally, related to the third point, sometimes the short hedge fails simply because the short instrument is actually quite different in nature than the long one, despite their superficial similarity. An example is provided by Mr. Sandy Fielden at Logical Information Machines. There is a usually profitable trade where you long a May gasoline futures contract and simultaneously short a May heating oil contract in the spring. The logic is that as the weather gets warmer, the driving season will begin which drives the price of gasoline futures up, and the demand for heating will decrease which drives the price of heating oil futures down. This hedged trade is supposed to eliminate general energy market risk. However, the weather is sometimes unpredictable, and in 2005, this trade went quite wrong primarily because the winter lasted longer. On the other hand, if you only enter the long side of this trade, i.e. buy gasoline futures in the spring, it works like a charm every year in the past 10 years! (I have posted a detailed analysis of this long-only gasoline futures trade in my Premium Content area.)

Therefore, if you trade for yourself and not for some institutions with a mandate only for market-neutral strategies, there is no need to be bounded by the same rules that they have to play by.

Saturday, March 24, 2007

Seven factors that capture most of hedge funds' returns

The Economist magazine just published an article that talked about "synthetic" hedge funds, or replicating hedge fund returns using factor models. The original research cited can be found here. (For those of you who want a primer on factor models, I have written an article on this topic previously.) The seven factors are (are you ready?):

1) excess return on the S&P 500 index;

2) a small minus big factor constructed as the difference of the Wilshire small and large

capitalization stock indices;

3) excess returns on portfolios of lookback straddle options on currencies;

4) excess returns on portfolios of lookback straddle options on commodities;

5) excess returns on portfolios of lookback straddle options on bonds;

6) the yield spread of the US ten year treasury bond over the three month T-bill, adjusted for the duration of the ten year bond;

7) the change in the credit spread of the Moody's BAA bond over the 10 year treasury bond, also appropriately adjusted for duration.

According to the researchers, factors 3)-5) are constructed to replicate the maximum possible return to trend-following strategies on their respective underlying assets.

See, it is not that difficult to run a hedge fund after all!

1) excess return on the S&P 500 index;

2) a small minus big factor constructed as the difference of the Wilshire small and large

capitalization stock indices;

3) excess returns on portfolios of lookback straddle options on currencies;

4) excess returns on portfolios of lookback straddle options on commodities;

5) excess returns on portfolios of lookback straddle options on bonds;

6) the yield spread of the US ten year treasury bond over the three month T-bill, adjusted for the duration of the ten year bond;

7) the change in the credit spread of the Moody's BAA bond over the 10 year treasury bond, also appropriately adjusted for duration.

According to the researchers, factors 3)-5) are constructed to replicate the maximum possible return to trend-following strategies on their respective underlying assets.

See, it is not that difficult to run a hedge fund after all!

Sunday, March 18, 2007

Is increasing beta or increasing leverage a better way to increase returns?

In my previous post, I reported an astute observation from my reader Mr. Goldstein that maximizing compound rate of return, maximizing leverage, and maximizing Sharpe ratio are all tightly connected. This makes intuitive sense because the higher the Sharpe ratio of a strategy, the smaller the drawdown, and therefore the higher the leverage you can apply to it in order to maximize compound return.

Mr. Goldstein also made another very interesting observation. He noted that there are usually 2 ways to increase the returns of a portfolio of stocks: either by picking high-beta stocks, or by increasing the leverage of the portfolio. In both cases, we are taking on more risk in order to generate more returns. But are these 2 ways equal? Or is one better than the other? It turns out that there is some research out there which suggests increasing leverage is the better way, due to the fact that the market seems to be chronically under-pricing high-beta stocks. This gives rise to a strategy called "Beta Arbitrage": buy low-beta stocks, short high-beta stocks, and earn a positive return.

I myself have not studied this form of arbitrage in depth, and therefore can neither endorse nor criticize it. However, if this research is correct, it does argue against including too many volatile stocks in your portfolio or trading strategy. If you want to take on more risk and generate higher return, just turn the knob and increase your leverage and therefore book size.

Mr. Goldstein also made another very interesting observation. He noted that there are usually 2 ways to increase the returns of a portfolio of stocks: either by picking high-beta stocks, or by increasing the leverage of the portfolio. In both cases, we are taking on more risk in order to generate more returns. But are these 2 ways equal? Or is one better than the other? It turns out that there is some research out there which suggests increasing leverage is the better way, due to the fact that the market seems to be chronically under-pricing high-beta stocks. This gives rise to a strategy called "Beta Arbitrage": buy low-beta stocks, short high-beta stocks, and earn a positive return.

I myself have not studied this form of arbitrage in depth, and therefore can neither endorse nor criticize it. However, if this research is correct, it does argue against including too many volatile stocks in your portfolio or trading strategy. If you want to take on more risk and generate higher return, just turn the knob and increase your leverage and therefore book size.

Sunday, March 04, 2007

Maximizing Compound Rate of Return vs Maximizing Sharpe ratio

A reader, Mr. A. Goldstein, made a very useful observation about my article "Maximizing Compound Rate of Return". In that article I argued that if your goal is to maximize the compound rate of return, you should maximize the quantity m – s2/2, where m is the short-term (1-period) rate of return, and s is its standard deviation. In general, this is not the same as maximizing the Sharpe ratio of a strategy. However, Mr. Goldstein pointed out that, if you also optimize the leverage of your strategy using Kelly's criterion, then maximizing Sharpe ratio does in fact maximize the compound rate of return also. This follows from a calculation in section 7 of Dr. Edward Thorpe's paper www.bjmath.com/bjmath/thorp/paper.htm.

Mr. Goldstein also suggested a beta arbitrage strategy which he has allowed me to share with my readers in a future post.

Mr. Goldstein also suggested a beta arbitrage strategy which he has allowed me to share with my readers in a future post.

Tuesday, February 27, 2007

Platinum-gold spread revisited

Now that Chinese New Year is over, it is time to revisit the Platinum-Gold spread that I talked about last November. The theory is that with the demand for gold seasonally exhausted due to the end of Asian festivities, gold prices will decline relative to platinum. We now have the opportunity to test this theory again.

Saturday, February 24, 2007

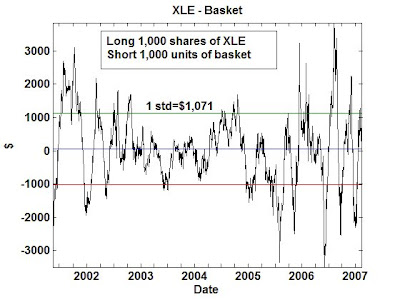

Index arbitrage with XLE

In looking for pairs of financial instruments to pair trade, we do not have to limit ourselves to pairs that occur in "nature". We can often construct our own baskets of stocks to trade against an index (or an ETF representing this index). In fact, such pairs usually show better cointegration properties than any stock or ETF pairs. I have alluded to this index arbitrage idea in an earlier post, and the details of the methodology are explained in my articles for Subscribers. I tried this strategy on favorite sector ETF: the energy SPDR XLE.

XLE is composed of some 33 stocks (as of 2/16/2007). Our goal is to pick some smaller subset of these stocks to form a basket. We pick them based on how well they cointegrate with XLE. How big should this subset be? The higher the number, the better this basket cointegrates with XLE, but the smaller the profits. (If you include all stocks in XLE in this basket, then the basket cointegrates perfectly with XLE, but there will be no trading opportunities!) The lower the number, the higher the (specific) risk as well as return. So it is more of a personal risk-return preference than any scientific criterion which determines how many stocks to pick. I pick a basket with 10 stocks. I have found that this basket cointegrates with XLE with better than 99% probability since 2001/05/22. The half-life for mean-reversion is about 20 days, which means you have to hold a position for at most a quarter. (My own rule is to exit when the spread hasn't reverted in 3 times the half-life.) If you enter into a position when the z-score is about ±2, you can expect a profit of about $2,000 on an investment of about $58,000 on one side. This comes to a return per trade of about 3%. You can of course boost this return by using options to implement the XLE position instead.

As an aside, if you use Interactive Brokers, you can easily trade an entire basket of stocks using their Basket Trader.

I have created an online spreadsheet with (almost) real-time values of this spread in the subscription area. (The detailed composition of this basket of 10 stocks are also described there.) Note that in theory, every time the XLE changes composition, we will have to re-compute our basket composition as well. But fortunately XLE composition does not change very much or very often, so I will only update my basket at most once a month.

XLE is composed of some 33 stocks (as of 2/16/2007). Our goal is to pick some smaller subset of these stocks to form a basket. We pick them based on how well they cointegrate with XLE. How big should this subset be? The higher the number, the better this basket cointegrates with XLE, but the smaller the profits. (If you include all stocks in XLE in this basket, then the basket cointegrates perfectly with XLE, but there will be no trading opportunities!) The lower the number, the higher the (specific) risk as well as return. So it is more of a personal risk-return preference than any scientific criterion which determines how many stocks to pick. I pick a basket with 10 stocks. I have found that this basket cointegrates with XLE with better than 99% probability since 2001/05/22. The half-life for mean-reversion is about 20 days, which means you have to hold a position for at most a quarter. (My own rule is to exit when the spread hasn't reverted in 3 times the half-life.) If you enter into a position when the z-score is about ±2, you can expect a profit of about $2,000 on an investment of about $58,000 on one side. This comes to a return per trade of about 3%. You can of course boost this return by using options to implement the XLE position instead.

As an aside, if you use Interactive Brokers, you can easily trade an entire basket of stocks using their Basket Trader.

I have created an online spreadsheet with (almost) real-time values of this spread in the subscription area. (The detailed composition of this basket of 10 stocks are also described there.) Note that in theory, every time the XLE changes composition, we will have to re-compute our basket composition as well. But fortunately XLE composition does not change very much or very often, so I will only update my basket at most once a month.

Thursday, February 15, 2007

Do Gold and Oil Cointegrate?

I have written extensively here about cointegration between gold-miners and gold ETF's (GDX vs GLD), as well as between energy companies and oil ETF's (XLE vs USO). (See, for e.g., this article, or this article.) On another occasion, I also commented on an Economist magazine article about the possible cointegration between bond yield and oil prices. However, my fellow blogger Yaser recently pointed out an interesting link between gold and oil also. The reasons why gold and oil may be cointegrated are very similar to that of bond yield and oil: as oil price rise a) the oil revenue is invested heavily in gold, therefore pushing up gold price; b) there is an upward pressure on inflation, which increases the appeal of gold as an inflation hedge.

I did a cointegration analysis between gold and oil prices, and though their spread certainly looks somewhat mean-reverting since the 90's, it doesn't pass the cointegration test. The reason may simply be that this spread mean-reverts at a glacial pace: I estimate that the half-life (see my explanation of this term here) is over 14 months. Therefore, it may require historical data back to the 1970's to convince ourselves of their cointegration. (My own data on crude oil and gold prices only go as far back as the 1990's. If any reader knows of historical data source that goes back further, please let me know.) If, however, one is willing to take their cointegration by faith despite the inadequate data, then one may believe that gold is currently (as of Feb 12, 2007) just slightly undervalued relative to oil (the spread is about $8). I certainly don't recommend entering into a position on either side at this point!

I did a cointegration analysis between gold and oil prices, and though their spread certainly looks somewhat mean-reverting since the 90's, it doesn't pass the cointegration test. The reason may simply be that this spread mean-reverts at a glacial pace: I estimate that the half-life (see my explanation of this term here) is over 14 months. Therefore, it may require historical data back to the 1970's to convince ourselves of their cointegration. (My own data on crude oil and gold prices only go as far back as the 1990's. If any reader knows of historical data source that goes back further, please let me know.) If, however, one is willing to take their cointegration by faith despite the inadequate data, then one may believe that gold is currently (as of Feb 12, 2007) just slightly undervalued relative to oil (the spread is about $8). I certainly don't recommend entering into a position on either side at this point!

{kind=link}

Wednesday, February 14, 2007

Another article on political futures markets

A NYTimes article yesterday talked about the political futures market intrade.com in the context of the November election, particularly the Virginia Senate race, which I blogged about before. I urged my readers to curb their enthusiasm for using such markets for prediction in my article, while the NYTimes article is certainly much more enamored of them. However, I think we can all agree that such markets are very efficient in synthesizing all existing information and opinion in making a prediction, but it cannot reveal information that nobody can possibly know at this point, such as who is going to win the 2008 general election.

Monday, February 12, 2007

Use the right discount rate to avoid jail time

Here is a fascinating story about the former treasurer of Essex County, New Jersey, who was sentenced to seven and a half years in prison because the prosecutor used the wrong discount rate to value certain tax-exempt bonds.

Saturday, February 10, 2007

In praise of day-trading

A recent article by Mark Hulbert in the NYTimes talked about the Value Line's rankings, and how this system is under-performing the market index in recent years. Mr. Hulbert asked Professor David Aronson of Baruch College whether this drop in performance means that the system has stopped working. Prof. Aronson says no: he believes that it takes 10 or more years [my emphasis] of under-performance of this strategy before one can say that it has stopped working! This statement, if taken out-of-context, is so manifestly untrue that it warrants some elaboration.

To evaluate whether a strategy has failed bears a lot of resemblance to evaluating whether a particular trade has failed. In my previous article on stop-loss, I outlined a method to determine how long it takes before we should exit a losing trade. This has to do with the historical average holding period of similar trades. This kind of thinking can also be applied to a strategy as a whole. If your strategy, like the Value Line system, holds a position for months or even years before replacing it with others, then yes, it may take many years to find out if the system has finally stopped working. On the other hand, if your system holds a position for just hours, or maybe just minutes, then no, it takes only a few months to find out! Why? Those who are well-versed in statistics know that the larger the sample size (in this case, the number of trades), the smaller the percent deviation from the mean return.

Which brings me to day-trading. In the popular press, day-trading has been given a bad-name. Everyone seems to think that those people who sit in sordid offices buying and selling stocks every minute and never holding over-night positions are no better than gamblers. And we all know how gamblers end up, right? Let me tell you a little secret: in my years working for hedge funds and prop-trading groups in investment banks, I have seen all kinds of trading strategies. In 100% of the cases, traders who have achieved spectacularly high Sharpe ratio (like 6 or higher), with minimal drawdown, are day-traders.

To evaluate whether a strategy has failed bears a lot of resemblance to evaluating whether a particular trade has failed. In my previous article on stop-loss, I outlined a method to determine how long it takes before we should exit a losing trade. This has to do with the historical average holding period of similar trades. This kind of thinking can also be applied to a strategy as a whole. If your strategy, like the Value Line system, holds a position for months or even years before replacing it with others, then yes, it may take many years to find out if the system has finally stopped working. On the other hand, if your system holds a position for just hours, or maybe just minutes, then no, it takes only a few months to find out! Why? Those who are well-versed in statistics know that the larger the sample size (in this case, the number of trades), the smaller the percent deviation from the mean return.

Which brings me to day-trading. In the popular press, day-trading has been given a bad-name. Everyone seems to think that those people who sit in sordid offices buying and selling stocks every minute and never holding over-night positions are no better than gamblers. And we all know how gamblers end up, right? Let me tell you a little secret: in my years working for hedge funds and prop-trading groups in investment banks, I have seen all kinds of trading strategies. In 100% of the cases, traders who have achieved spectacularly high Sharpe ratio (like 6 or higher), with minimal drawdown, are day-traders.

Monday, February 05, 2007

Index tracking, arbitrage, and cointegration

Mr. Lange, a reader of mine from Germany, alerted me to the following paper regarding a strategy related to index arbitrage that involves the EUROStoxx50 index. It is a nice illustration of a common application of cointegration techniques to statistical arbitrage trading. I have written an exposition of this paper, together with an additional index arbitrage strategy not discussed in the original paper, which I posted to my subscribers only area. (Mr. Lange has graciously allowed me to share this exposition with other readers of this blog.)

Sunday, February 04, 2007

Cointegration between oil and bond yield? Not!

An article in the Feb 1 issue of the Economist magazine suggested that there may be a link between crude oil price and long-dated US treasuries. Their reasoning is that if oil price is high, OPEC will need to re-invest the pile of cash that they generate, and eventually a lot of this ended up invested in US 10-year bond. Therefore, when crude prices go up, 10-year yield should go down. As I explained before, the fact that these 2 numbers are anti-correlated do not prevent them from being cointegrated. And in fact, the Economist article plotted the crude oil prices together with bond yield over the last year together, and they seem tantalizingly close to being cointegrated.

My curiosity piqued, I proceeded to get a longer history of these data to examine.

In the graph above, I plotted the (normalized) difference between the 10-year treasury yield and oil price. One can see that over the last year and a half, they are indeed cointegrated to a good degree. (To see that, notice the spread is range-bound, or mean-reverting, from mid-2005 to the present.) But this relationship breaks down completely over the longer history.

In the graph above, I plotted the (normalized) difference between the 10-year treasury yield and oil price. One can see that over the last year and a half, they are indeed cointegrated to a good degree. (To see that, notice the spread is range-bound, or mean-reverting, from mid-2005 to the present.) But this relationship breaks down completely over the longer history.

Though I think that the Economist magazine is doing a disservice to its readers for plotting this graph over just one year and making innuendos of linkage, it is a nice illustration of the danger of studying cointegration over a short window.

My curiosity piqued, I proceeded to get a longer history of these data to examine.

In the graph above, I plotted the (normalized) difference between the 10-year treasury yield and oil price. One can see that over the last year and a half, they are indeed cointegrated to a good degree. (To see that, notice the spread is range-bound, or mean-reverting, from mid-2005 to the present.) But this relationship breaks down completely over the longer history.

In the graph above, I plotted the (normalized) difference between the 10-year treasury yield and oil price. One can see that over the last year and a half, they are indeed cointegrated to a good degree. (To see that, notice the spread is range-bound, or mean-reverting, from mid-2005 to the present.) But this relationship breaks down completely over the longer history.Though I think that the Economist magazine is doing a disservice to its readers for plotting this graph over just one year and making innuendos of linkage, it is a nice illustration of the danger of studying cointegration over a short window.

Sunday, January 28, 2007

Stop-loss strategy: re-post

Due to a technical glitch, many subscribers to this blog were not notified of my latest article on stop-loss strategy and a method to estimate optimal holding period for mean-reverting strategies.

So here is the permanent link again.

So here is the permanent link again.

Monday, January 15, 2007

What is your stop loss strategy?

A reader recently asked me whether setting a stop loss for a trading strategy is a good idea. I am a big fan of setting stop loss, but there are certainly myriad views on this.

One of my former bosses didn't believe in stop loss: his argument is that the market does not care about your personal entry price, so your stop price may be somebody else’s entry point. So stop loss, to him, is irrational. Since he is running a portfolio with hundreds of positions, he doesn’t regard preserving capital in just one or a few specific positions to be important. Of course, if you are an individual trader with fewer than a hundred positions, preservation of capital becomes a lot more important, and so does stop loss.

Even if you are highly diversified and preservation of capital in specific positions is not important, are there situations where stop loss is rational? I certainly think that applies to trend-following strategies. Whenever you incur a big loss when you have a trend-following position, it ususally means that the latest entry signal is opposite to your original entry signal. In this case, better admit your mistake, close your position, and maybe even enter into the opposite side. (Sometimes I wish our politicians think this way.) On the other hand, if you employ a mean-reverting strategy, and instead of reverting, the market sticks to its original direction and causes you to lose money, does it mean you are wrong? Not necessarily: you could simply be too early. Indeed, many traders in this case will double up their position, since the latest entry signal in this case is in the same direction as the original one. This raises a question though: if incurring a big loss is not a good enough reason to surrender to the market, how would you ever decide if your mean-reverting model is wrong? Here I propose a stop loss criterion that looks at another dimension: time.

The simplest model one can apply to a mean-reverting process is the Ornstein-Uhlenbeck formula. As a concrete example, I will apply this model to the commodity ETF spreads I discussed before that I believe are mean-reverting (XLE-CL, GDX-GLD, EEM-IGE, and EWC-IGE). It is a simple model that says the next change in the spread is opposite in sign to the deviation of the spread from its long-term mean, with a magnitude that is proportional to the deviation. In our case, this proportionality constant θ can be estimated from a linear regression of the daily change of the spread versus the spread itself. Most importantly for us, if we solve this equation, we will find that the deviation from the mean exhibits an exponential decay towards zero, with the half-life of the decay equals ln(2)/θ. This half-life is an important number: it gives us an estimate of how long we should expect the spread to remain far from zero. If we enter into a mean-reverting position, and 3 or 4 half-life’s later the spread still has not reverted to zero, we have reason to believe that maybe the regime has changed, and our mean-reverting model may not be valid anymore (or at least, the spread may have acquired a new long-term mean.)

Let’s now apply this formula to our spreads and see what their half-life’s are. Fitting the daily change in spreads to the spread itself gives us: