By Sergei Belov, Ernest Chan, Nahid Jetha, and Akshay Nautiyal

We applied

Corrective AI (Chan, 2022) to a trading model that takes

advantage of the intraday seasonality of forex returns. Breedon and Ranaldo

(2012) observed that foreign currencies

depreciate vs. the US dollar during their local working hours and appreciate

during the local working hours of the US dollar. We first backtested the

results of Breedon and Ranaldo on recent EURUSD data from September 2021 to

January 2023 and then applied Corrective AI to this trading strategy to achieve

a significant increase in performance.

Breedon and Ranaldo (2012) described a trading

strategy that shorted EURUSD during European working hours (3 AM ET to 9 AM ET,

where ET denotes the local time in New York, accounting for daylight savings)

and bought EURUSD during US working hours (11 AM ET to 3 PM ET). The rationale

is that large-scale institutional buying of the US dollar takes place during

European working hours to pay global invoices and the reverse happens during US

working hours. Hence this effect is also called the “invoice effect".

There is some supportive evidence for the

time-of-the-day patterns in various measures of the forex market like

volatility (see Baille and Bollerslev(1991), or Andersen and Bollerslev(1998)),

turnover (see Hartman (1999), or Ito and Hashimoto(2006)), and return (see

Cornett(1995), or Ranaldo(2009)). Essentially,

local currencies depreciate during their local working hours for each of these

measures and appreciate during the working hours of the United States.

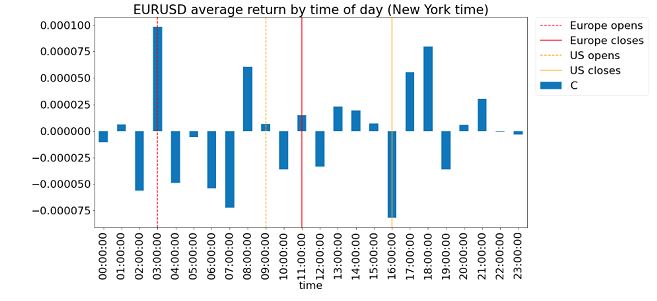

Figure 1 below describes the average hourly

return of each hour in the day over a period starting from 2019-10-01 17:00 ET

to 2021-09-01 16:00 ET. It reveals the pattern of returns in EURUSD. The return

pattern in the above-described “working hours'' reconciles with the hypothesis

of a prevalent “invoice effect” broadly. Returns go down during European

working and up during US working hours.

Figure

1: Average EURSUD return by time of day (New York time)

As this strategy was published in 2012, it

offers ample time for true out-of-sample testing. We collected 1-minute bar

data of EURUSD from Electronic Broking Services (EBS) and performed a backtest

over the out-of-sample period October 2021-January 2023. The Sharpe Ratio of

the strategy in this period is 0.88,

with average annual returns of 3.5% and a maximum drawdown of -3.5%. The alpha

of the strategy apparently endured. (For the purpose of this article, no

transaction costs are included in the backtest because our only objective is to

compare the performances with and without Corrective AI, not to determine if

this trading strategy is viable in live production.)

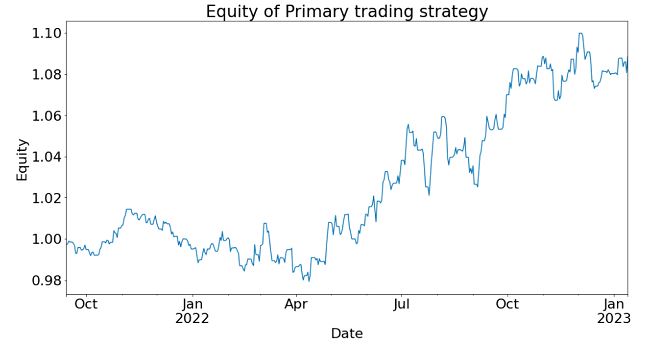

Figure 2 below shows the equity curve (“growth

of $1”) of the strategy during the aforementioned out-of-sample period. The

cumulative returns during this period are just below 8%. We call this the

“Primary” trading strategy, for reasons that will become clear below.

Figure

2: Equity curve of Primary trading strategy in out-of-sample period

What is

Corrective AI?

Suppose

we have a trading model (like the Primary trading strategy described above) for

setting the side of the bet (long or short). We just need to learn the size of

that bet, which includes the possibility of no bet at all (zero sizes). This is

a situation that practitioners face regularly. A machine learning algorithm

(ML) can be trained to determine that. To emphasize, we do not want the ML

algorithm to learn or predict the side, just to tell us what is the appropriate

size.

We

call this problem meta-labeling (Lopez de Prado, 2018) or Corrective AI (Chan,

2022) because we want to build a secondary ML model that learns how to use a

primary trading model.

We

train an ML algorithm to compute the “Probability of Profit” (PoP) for the next

minute-bar. If the PoP is greater than 0.5, we will set the bet size to 1;

otherwise we will set it to 0. In other words, we adopt the step function as

the bet sizing function that takes PoP as an input and gives the bet size as an

output, with the threshold set at 0.5.

This bet sizing function decides whether to take the bet or pass, a

purely binary prediction.

The

training period was from 2019-01-01 to 2021-09-30 while the out-of-sample test

period was from 2021-10-01 to 2023-01-15, consistent with the out-of-sample

period we reported for the Primary trading strategy. The model used to train ML

algorithm was done using the predictnow.ai Corrective AI (CAI) API, with more

than a hundred pre-engineered input features (predictors). The underlying

learning algorithm is a gradient-boosting decision tree.

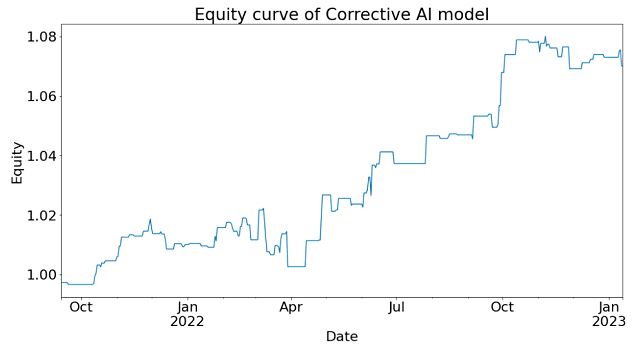

After applying Corrective AI, the Sharpe Ratio

of the strategy in this period is 1.29

(an increase of 0.41), with average annual returns of 4.1% (an increase

of 0.6%) and a maximum drawdown of -1.9%

(a decrease of 1.6%). The alpha of the strategy is significantly improved.

The equity curve of the Corrective AI filtered

secondary model signal can be seen in the figure below.

Figure

3: Equity curve of Corrective AI model

in out-of-sample period

Features used to train the Corrective AI model include technical

indicators generated from indices, equities, futures, and options markets. Many

of these features were created using Algoseek’s high-frequency futures and equities

data. More discussions of these features can be found in (Nautiyal & Chan,

2021).

Conclusion:

By applying Corrective AI to the

time-of-the-day Primary strategy, we were able to improve the Sharpe ratio and

reduce drawdown during the out-of-sample backtest period. This aligns with

observations made in the literature on meta-labeling for our primary

strategies. The Corrective AI model's signal filtering capabilities do enhance

performance in specific scenarios.

Acknowledgment

We are grateful to Chris Bartlett of Algoseek,

who generously provided much of the high-frequency data for our feature

engineering in our Corrective AI system. We also thank Pavan Dutt for his

assistance with feature engineering and to Jai Sukumar for helping us use the

Predictnow.ai CAI API. Finally, we express our appreciation to Erik MacDonald

and Jessica Watson for their contributions in explaining this technology to

Predictnow.ai’s clients

References

Breedon,

F., & Ranaldo, A. (2012, April 3). Intraday

Patterns in FX Returns and Order Flow. https://ssrn.com/abstract=2099321

Chan,

E. (2022, June 9). What is Corrective AI?

PredictNow.ai. Retrieved February 23, 2023, from

https://predictnow.ai/what-is-corrective-ai/

Lopez

de Prado, M. (2018). Advances in

Financial Machine Learning. Wiley.

Nautiyal,

A., & Chan, E. (2021). New Additions

to the PredictNow.ai Factor Zoo. PredictNow.ai. Retrieved February 28,

2023, from https://predictnow.ai/new-additions-to-the-predictnow-ai-factor-zoo/